I‘ve had a good run for flipping homes over the past five years. Thanks to the subprime fiasco, the nation’s economy tanked, home prices fell, interest rates took a nosedive to historic lows, and inventory was plentiful — especially in the foreclosure market. I’ve been able to pick up REO properties at a good discount, then renovate and get a healthy profits on resale.

But recently the market is shifting and the ability to buy distressed homes at a low enough discount to earn a healthy profit is starting to diminish. It seems that the banks are releasing less REO inventory and what is put on the market is getting picked up quickly either by hedge funds or even the savvy owner/occupant looking for a bargain. Many of the REO properties are coming online with some basic renovations already completed by the banks. This trend has been recognized by my peers here in western Washington as well as others across the country.

Fortunately I keep my head above the weeds and see what other opportunities there are in the distressed real estate landscape. Last year I found myself at note conferences learning about the nonperforming note business and I’ve started into this niche “full steam ahead” in 2014. I’m still flipping homes — but my longer range goal is to transition into repositioning nonperforming notes as my primary business model. With less interdependencies and a higher upside, it just makes good sense. By repositioning distressed mortgage debt I not only help increase my investor’s bottom line, the homeowner has the opportunity to stay in their home and avoid foreclosure. It’s a win/win that the large financial institutions cannot execute well.

By repositioning distressed mortgage debt I not only help increase my investor’s bottom line, the homeowner has the opportunity to stay in their home and avoid foreclosure.

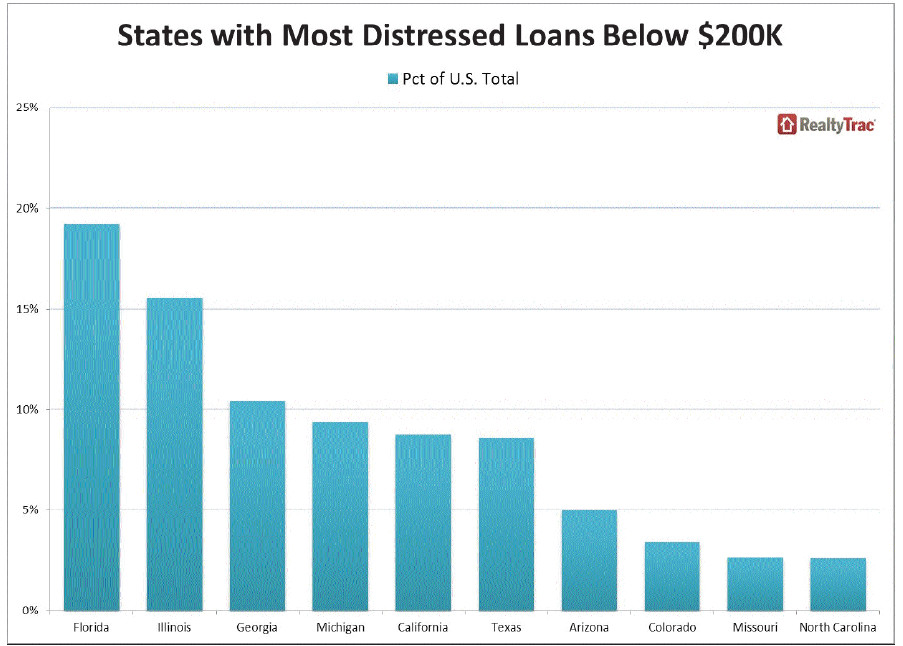

At a recent presentation by Eddie Speed, a veteran note buyer, he pointed out that there are approximately 400,000 REO’s in banks inventory but nearly 2 million notes over 90 days delinquent. This is what is now known as the “shadow inventory”. Eddie’s analysis really opened my eyes to the larger picture and what is driving the reduction in available REOs to flip. With lenders now unloading their nonperforming notes “by the truckload”, it is a good time to change gears.

Notes are appealing because they offer less competition from other investors — even the large investors backed by big Wall Street funds —when compared to buying real property. Factor in the low inventory of available homes for sale, both traditional homes and bank-owned properties (REOs), and the note business becomes even more attractive. Similar to owning real property, notes can be repositioned for cashflow and even resold to another note buyer at a profit– without the risks associated with real property, like tenants, repairs, taxes, financing, etc.

With literally hundreds of thousands of note deals out there, investors just need to know where to find the opportunities and do the deals. I’ve already purchased 4 nonperforming notes and plan to acquire more as the opportunities arise.

To get an idea of how the shadow inventory was created, watch this video on how Fannie Mae securitization works: