Many investors are seeking diversity in their portfolios and the income stream from a mortgage payment is one of the most desirable asset classes.

Why? Mortgage notes have some if the most appealing qualities, including:

- The loan is backed by a hard asset: real estate.

- Typically the loan will be purchased at a discount to the value of the home. This provides a built in equity cushion as a margin of safety should the home’s value decline in a recession.

- The note holder can foreclose on the home should the borrower default. If there is equity between the note payoff balance and the value of the home, the note holder will receive 100% of their investment capital, and perhaps more if there were unpaid arrearages.

- Aside from default, a solid performing note provides a steady stream of income to the note investor. Getting a monthly payment from the loan servicer is a great way to build wealth in a Self Directed IRA.

Now one of the frequent problems that a note investor faces is having sufficient capital to purchase the note. Unlike owning the home, it is unlikely that the investor can use leverage to acquire a note, so this is a cash intensive proposition.

Solution: The Partial Term Purchase

Even though the remaining balance and term may be more than an investor can allocate to a whole note purchase, the note holder can offer to sell a fixed amount of payments due on a note. The investor is buying part of the remaining term, known as a “partial”. Let’s review how this works:

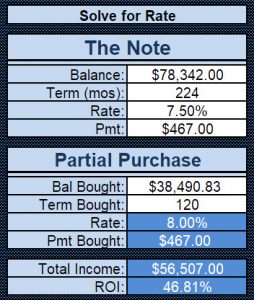

Note Info:

This is a first position note on a 3/2 single family home. Debtor has made 14 monthly payments on time.

Property Value: $110,000

UPB: $78,342

Loan Rate: 7.5%

Maturity Date: 8/1/2035

Remaining Term: 224 months

Monthly P&I: $467.00

The investor purchases the next 120 month’s of P&I payments of $467/month for $38,490.83. Investor’s annualized yield is 8% and the total ROI over the 120-month period is 46.81%

The investor purchases the next 120 month’s of P&I payments of $467/month for $38,490.83. Investor’s annualized yield is 8% and the total ROI over the 120-month period is 46.81%At the end of the partial term the note is assigned back to the seller/note investor who then receives the remaining 104 monthly P&I payments.

What happens if the debtor defaults during the partial term?

The sale of a partial term is usually completed using a fully executed receivables assignment agreement. This agreement will have specific terms to determine what happens should the debtor default during the term. In most contracts the note investor/seller will have the option or requirement to buy back the note and complete loss mitigation with the debtor.

The benefit for purchasing partial terms

The purchase of a partial term is an excellent way for a Self Directed IRA to easily acquire a cash flow stream, backed by real estate, with the protections provisioned by the receivables agreement.

To find out more about partials and what inventory we have available, please click here and complete our contact form. Please be sure to indicate that you are interested in partials and what your current budget is for purchase.

Below is a video from my partner Josh Andrews which goes into more dept about partial loan payments.