The Opportunity With Distressed Notes

Purchasing distressed notes is an excellent way to help borrowers who have “underwater” homes stay in their home by modifying their loan to terms that they can afford. Since financial institutions are unloading their “bad debt” this provides an opportunity to invest in real estate without having to actually manage the property secured by the debt. Essentially, the sale of distressed notes is the sale of debt obligations for property. For example, if a mortgage is for $100,000 and the borrower is currently unable to pay, the bank may sell the mortgage for $50,000 in order to get at least some of its money back.

Why? Banks are in the business of lending money, not owning and operating real estate. By selling the note rather than going through the expensive and sometimes drawn out process of foreclosing, a bank stays out of the chain of title, doesn’t become liable for the property’s environmental conditions and doesn’t have to worry about the time—and expense—of other property management and ownership issues. Add in the cost and effort of marketing the property to potential buyers following the foreclosure and the numerous existing properties already being carried on their books, and you can see why banks were looking for an alternative to foreclosures. Selling its debt has provided that alternative avenue.

We the obvious benefit of purchasing distressed notes — the opportunity to obtain the loan and underlying property at a steep discount from its initial price. This discount provides a high margin for potential profit on the note depending upon how we reposition the debt with the borrower, and provides the borrower an opportunity to remain in their home and avoid foreclosure.

Due Diligence And Repositioning

Although purchasing distressed or nonperforming notes can be a highly lucrative asset class, the same level of due diligence is required to evaluate the note based both on the characteristics of the note as well as the property on which it is secured. The type of diligence that we perform in any real estate transaction depends upon both the type of transaction and the kind of asset which is being purchased or encumbered. Typically it involves review of the note, deed of trust, chain of title, unpaid taxes/liens and borrowers affordability and willingness to stay in their home.

After due diligence and the successful acquisition of the note, we can then “reposition” the note, essentially transforming it from a nonperforming asset into a performing asset. This is done by working with the borrower to modify the parameters of the note to provide them a reasonable plan to resume their payments on the debt. Commonly known as a loan modification, we can change the interest rate, the length of the loan term or even the amount of the loan to better match the borrower’s payment ability. This allows the borrower to avoid foreclosure by resuming their debt payments and provides us income on an asset that was previously considered a liability.

Performance From Repositioned Notes

Once we establish an agreement with the borrower and performance has been established, an income stream is realized from the repositioned note, converting it from a distressed note to a performing asset. We then have the flexibility to hold the note for income or we can liquidate the repositioned & performing note to another investor at a discount of face value, realizing a profit from our acquisition and repositioning costs, and generating new capital to reinvest in new distressed notes or value-added properties.

Once we establish an agreement with the borrower and performance has been established, an income stream is realized from the repositioned note, converting it from a distressed note to a performing asset. We then have the flexibility to hold the note for income or we can liquidate the repositioned & performing note to another investor at a discount of face value, realizing a profit from our acquisition and repositioning costs, and generating new capital to reinvest in new distressed notes or value-added properties.

Market Opportunities

The volume of non-performing real estate loans has picked up dramatically over the past 5 years as banks seek to shrink their balance sheets as their capital base falls. In both multifamily and residential real estate, there are now billions of dollars worth of outstanding, distressed debt. Whereas a few years ago, banks would have been more inclined to foreclose on a non-performing property, they are now choosing to sell the note. The primary reason is that for each dollar that a bank has on its books in loans, they are required by the federal government to keep anywhere from 6 to 10-times the amount in reserves. Now that these notes are climbing into the billions, banks are now willing to unload nonperforming notes to recover their capital reserves.

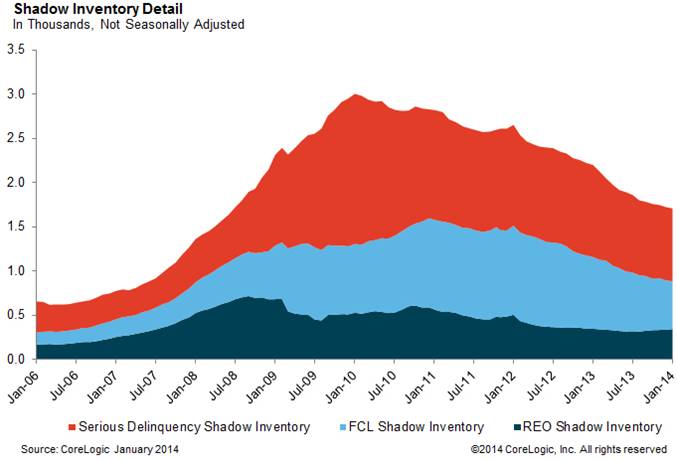

According to CoreLogic, the “shadow inventory” has declined since the peak in 2010, but there is a substantial inventory of loans still over 90-days delinquent. This is represented by the red section of the chart above. Financial institutions are reducing their bank owned (REO) sales as indicated by the dark blue section and keeping them in reserve due to cost considerations and to avoid market dilution. This indicates that a huge inventory of distressed mortgages remains on the books for lenders. See the full report from the Federal Reserve Bank of NY here.