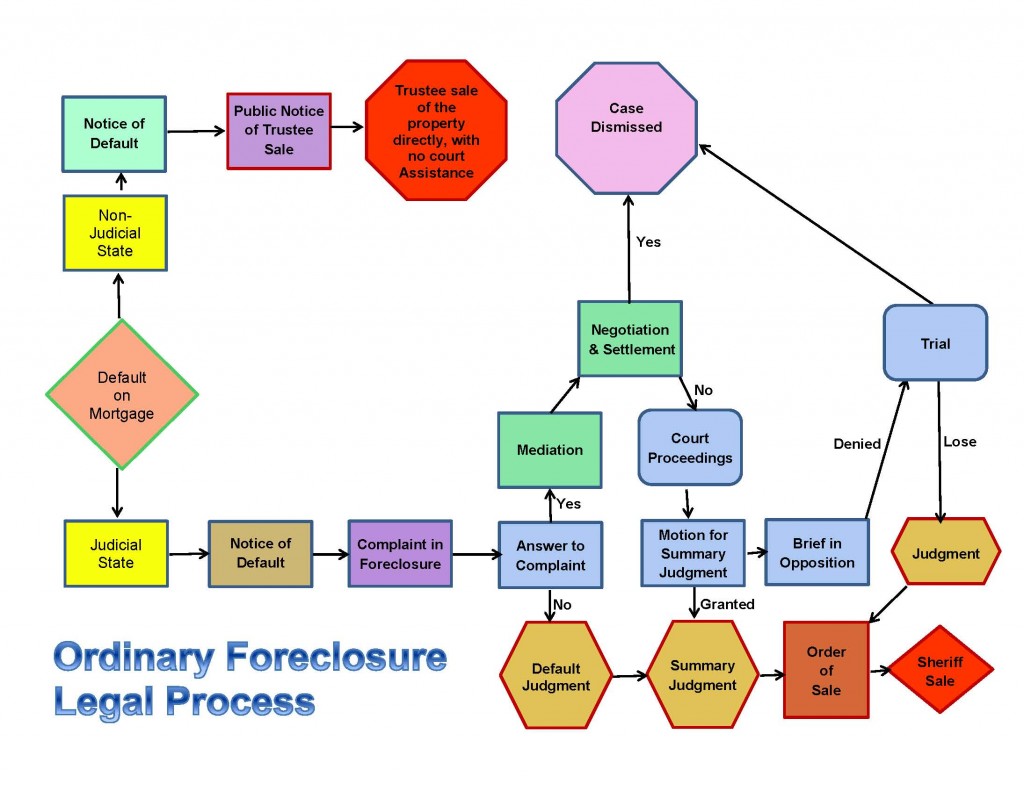

Below is an overview of the foreclosure process for both judicial and non judicial states. If we have a venture with a loan in foreclosure, please use the info below as a reference guide for procedures and timing.

1.) The first thing we do is try to obtain a loan modification, reinstatement, forbearance, and-or principal reduction to provide the borrower an opportunity to stay in their home.

2.) The second thing we can do is allow a foreclosure alternative like a short sale, or deed-in lieu of foreclosure (DIL). In these solutions, the property being returned to us. In many instances, these foreclosure alternatives include offers cash for keys, lease back, deficiency relief, and more.

Understanding the Foreclosure Process – Foreclosure Types

Foreclosures come in two types: judicial and non-judicial.

A judicial foreclosure is a process wherein we must use the court system to seize the home. This makes foreclosure more expensive for us, and can typically take much longer to complete.

A non-judicial foreclosure, on the other hand, is based on the state’s statutory requirements. In this foreclosure process, we don’t have to go through the court system to foreclose on a home. This kind of foreclosure can take as little as three months. Many non-judicial foreclosure states have recently adopted procedures that require foreclosures to be approved by a judge, in order to protect homeowners’ rights. In these states, it is now even more important than ever to hire a foreclosure defense attorney.

Below is a description of the process taken from the borrower’s position.

Understanding the Foreclosure Process – Notice of Default (NOD)

In either case, once your lender decides to foreclose, they will record a Notice of Default (NOD) at the county office where your home is located. This usually doesn’t happen until you miss your third payment, but once it does, it progresses fairly quickly. Within 10 days, your lender will publish the NOD in the local newspaper and, within 30 days, you should receive the same notice by mail. Once you have received a notice of default, only a foreclosure defense attorney can effectively protect your interests.

The NOD outlines the steps you need to take to resolve the defaulted mortgage. Most lenders give you three months to bring account current. Otherwise, your lender can schedule a sale date and your house can be sold within the next month. Once your home is sold, you have ten days to leave the property.

When you fall behind in your mortgage payments, you can expect lenders to react in specific ways at specific times. There are also two distinct foreclosure processes; judicial and non-judicial. While not all lenders use the same process, the following timeline shows a typical foreclosure timeline, from late payment to foreclosure.

Understanding the Foreclosure Process- Typical Foreclosure Timeline

Day 1-15:

The Mortgage payment is due on the first of the month, and usually has a 15 day grace period. During this period, your payment is not yet “late”.

When the borrower misses a payment:

Day 16-30:

At this point, a late charge is assessed which is typically 5% of the monthly payment. The company that processes the payments (called the mortgage servicer) begins collection activities with attempts to contact with the borrower to find out why the payment is late. This is one of the the best times to request assistance, such as a loan modification.

Day 31:

At this point, the new month begins and a payment is due for both the previous month and the current month. Any payment you make will be applied to the previous month’s payment and late fees before being applied to the current month’s payment.

Day 46-60:

During this period, the servicer sends a “demand” or “breach” letter to the borrower explaining that the terms of the mortgage have been violated. The borrower is given 30 days to resolve the delinquency by paying the delinquent amount. The “escalation” clause of the Standard Federal Mortgage is now in effect. The lender/servicer can only accept payment in full of all outstanding mortgage payments, penalties, collection costs, and other legally allowable fees, or forfeit their rights to foreclose on the property.

Day 90: Notice of Default:

Foreclosure proceedings begin with a Notice of Default (NOD). The document is recorded in the county in which the property is located. The recording of the Notice of Default gives “Constructive Notice” to the public.

Day 120:

This is the latest time that a Complaint for Foreclosure will be filed in the court system. In a Judicial State, the homeowner must answer this civil suit, most often by using a foreclosure defense attorney. The defendant then has 28 days to respond or have a default judgment issued by the court against them. (In California, after the recording of the Notice of Default, the borrower and junior lien holders are given proper notification and the borrower has 90 days to bring their account current. This period is referred to as the Reinstatement Period.

Day 180:

Notice of Trustee Sale. If the borrower does not reinstate their account within the 90 day period, the lender will authorize and instruct the Trustee to record the Notice of Trustee Sale (NOS).

Day 201:

After 21 days of the recording of the NOS, a foreclosure sale can take place at public auction. (The property may be sold to a third party bidder or revert back to the lender for a specified amount.)

Trustee Sale (Sheriff Sale):

The property is scheduled for sale in as little as 60 days or as long as 300 days from filing. Bidders are required to pay with certified funds. The opening bid starts at two thirds, or 67%, of the sheriffs appraised value of the property. The auctioneer seeks the highest bid; the successful bidder must tender payment at the sale. In some states, there is a redemption period not longer than 30 days.